Few of the game’s core economic features figures to be as impactful in upcoming collective bargaining negotiations as the luxury tax (or competitive balance tax, as it’s officially known). Where to set the tax thresholds and what penalties should be in place for teams that exceed them are key points of issue for the league’s owners and the MLB Players Association.

As a brief primer, the luxury tax was first introduced for the 1997 season. The provision’s purpose is to deter spending among big-market franchises by penalizing teams that exceed certain player expenditures. (MLBTR’s Tim Dierkes covered the year-by-year progression of the luxury tax in a post earlier this month). Teams that surpass certain thresholds will be faced with financial penalties and potential draft choice/international signing bonus forfeitures, which become more significant for teams that exceed the threshold by particularly high margins and/or surpass the mark in multiple consecutive seasons. Teams’ CBT figures are calculated by summing the average annual values of their commitments and accounting for certain player benefits, not by looking at clubs’ actual payrolls in any given year.

For the 2021 season, the first luxury tax marker was set at $210MM. Only the Dodgers and Padres exceeded that figure. Five teams, meanwhile, curtailed their spending between $205MM and $210MM, seemingly treating the CBT threshold as some form of cap.

The three clubs that exceeded the threshold in 2020 (the Yankees, Astros and Cubs) all ducked underneath in 2021. That’s in continuation with a fairly common pattern for teams to “reset” their tax bracket after a year or two above the threshold, thereby avoiding the escalating penalties for exceeding in consecutive years.

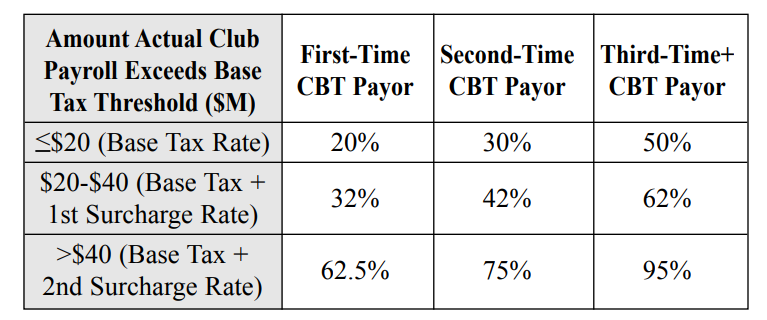

It’s not only resetters that stayed below the threshold though. The Phillies, Mets and Red Sox — none of whom exceeded the tax in 2020 — were within $5MM of the mark but decided against surpassing $210MM. MLBTR’s Tim Dierkes explored teams’ increasing reluctance to go over the tax threshold in February. Even for teams that didn’t have firm organizational mandates to stay below the mark, many were reluctant to take on any sort of penalty unless they were in position to blow by those markers, as both Mets owner Steve Cohen and Astros general manager James Click explained over the summer. The fees for exceeding the various thresholds under the 2016-21 CBA were as follows:

With certain high-payroll teams at least planning their budget with the luxury tax in mind — if not treating it as a firm cap altogether — pushing the thresholds up figures to be a point of emphasis for the players. After all, higher thresholds should lead to more willingness about the league’s top teams to spend. In collective bargaining talks before the lockout, the MLBPA proposed a $245MM threshold that would eliminate the escalating penalties for repeat payors, according to Gabe Lacques and Bob Nightengale of USA Today.

The league, predictably, hasn’t been as keen on increasing penalty-free spending capacity. MLB’s first core economics proposal actually called for the first tax threshold to be reduced to $180MM, as Ken Rosenthal and Evan Drellich of the Athletic reported in August. That came attached to a $100MM salary floor designed to incentivize spending among lower-payroll clubs, but the significantly lowered CBT thresholds always looked to be a non-starter for the union.

After the MLBPA rejected the $180MM possibility, the league offered to raise the tax thresholds above the $210MM level from 2021, albeit nowhere near the MLBPA’s target area. Shortly after the beginning of the lockout, Drellich reported the league was willing to push the first tax marker up to $214MM in the early years of a possible CBA, maxing out at $220MM by the end of the deal. That’s more in line with the gradual increases that have been in place in recent collective bargaining agreements than with the MLBPA’s push for a marked uptick.

There are a few different aspects for the league and union to agree upon regarding the competitive balance tax. Identifying a mutually-agreeable base number is the most obvious, but whether to reduce or eliminate penalties for repeat payors could be a point of contention. So too may be how the parties want to handle the escalating fees for clubs that exceed the marker by greater amounts. Indeed, the league’s initial proposal (the one which would’ve included a $180MM base tax threshold) also would’ve involved the creation of a fourth tier of penalization.

Ironing out the finer details of the luxury tax will be a challenge. Back-and-forth regarding the specifics of the CBT figures to be a recurring theme once the parties reinitiate discussions regarding core economics next month.

The fact that they haven’t even been meeting just absolutely pisses me off as a fan of baseball. I get there needs to be negotiations for it to be fair for both sides… but negotiations mean you actually need to meet up to talk. You’ve gone a month now of just sitting on your hands. If games are missed then it just goes to show the fans are not even a concern for both the players and the league.

Players union also seems far too relaxed about it… I understand that they are still getting paid but really? You’re not gonna get paid as much if you lose your fans…

The players are not getting paid right now but that is standard protocol as they only get paid during the regular season. The only people getting paid are those with buy outs or deferred salaries that have payment due dates in the offseason.

Oh. Got it

Don’t player union reps still get their wages as a union rep that are separate from their salary as a player like most union reps that are employees?

So the player reps are getting paid. Probably not too much (in MLB standards, but certainly a hefty sum compared to most union reps)

i can’t speak for all unions but the mid-america carpenters union (which is ka, mo, and il) the only ones that get paid are the ba’s and board members of the overall union but the officers at the locals don’t get paid or if they do it isn’t much because they all work in the field.

@TheBaseballFan

Did the players lock themselves out? They gave up too much in the last agreement. Plus the compensation and luxury tax are getting too complicated. If the players bend more the owners will change anything they can to increase profit. Implement 20 team playoffs, 20 layers of compensation for different revenue clubs.

This is just how the owners and front offices negotiate now. They sign guys last minute who are desperate. MLB is doing their version.

Umm 20 team playoffs? That would mean teams like the Royals would playing the White Sox or Blue jays in the Wild card series. I don’t logically see that happening

“The players gave up too much in the last CBA” is one of the favorite talking points for people on the internet who know nothing about the CBA or collective bargaining. The MLBPA has a great CBA. The tax thresholds have increased incrementally in every agreement and they will continue to increase incrementally. T’here will be no revolutionary increase in the luxury tax levels, and notwithstanding the desire of the MLBPA to return to the 1990’s the Competitive Balance Tax is here to stay. Both are good for the game and the owners aren’t going to agree to a radical change in either

The worst thing is that the MLBPA knows all this. They know the tax levels will increase incrementally, as they always do, rather than radically. But they are playing to the crowd, the agents who stab them in the back to the media, and the online bargaining ‘experts;’. Once the bubbles have all risen to the surface and burst, the MLBPA will be pushed to bargain a realistic deal or else have a 1990’s hockey strike that almost busts the union.

@baseballfan

Some owners only care about profits and more teams means more money.

People said we would never have as many teams as they have now. It’s not hard to see which way this trend is going.

The last CBA has been horrible for baseball. You say always like luxury taxes have been around for a long time. The CBT is welfare for billionaires and it doesn’t increase competitiveness. Fans like you are blaming the players even when the owners locked them out. Must be nice to be a billionaire

Of course they care about profits weirdo!… If you own a business, your goal is to maximize profits.

@forwhomthebelltolled

Seriously, what did the players “give up”? I seem to have forgotten. I know the CBT levels increased over the contract. (Pandemic being an unforseen circumstance) I know that a 26th player got added. More time off at the AS break. Please refresh my memory.

Then buy something else. Sports are different. They started as a way to bring pride to a city that had usually made the owners filthy rich.

No players are getting paid, and no one will get paid at all until there are MLB games.

It’s all about $$$, whether it’s the universal DH, expanded playoffs, CBT, or pitch clock. It’s all incentivized to make the players and owners more money. The fans and tradition of the game have become an afterthought with Manfred as commissioner.

Ehhh, despise the whole thing as much as anyone, but thats not really how these things happen. Its normally all done at once and not a long drawn out thing. Theyre really operating under the idea of a binary. “We need to get this done before next season, thats all that counts.” Youll see a lot more in late january and febuary. If stuff doesnt move then, thats when to be nervous.

On a side note, one of the things that is rarely talked about is that team owners should be talked about as having the privilege to own, not the power. MLB is a rare business where the growth is mostly dictated by the growth of the whole league or how winningest the team is. And its Mother @#%$#$%# protected!

Its also a product with a line from here to the moon of people that can afford to buy it off them. They own an annuity and theyre acting like they should be praised for being the one with their name on the door, they ARE NOT. why their investmetns are increasing (mostly)

They were given a gift, they are absolutely not doing anyone a favor. I cant name a single owner in modern pro sports who came out poorer than when he went in. There are almost no businesses like that and the media should write about owners that way.

@bkbk, YES! You nailed it my friend. This is why I am pro-player in the MLBPA vs. MLB/owners dynamic. Owners net worths’ go up year after year regardless of Tix sales, concessions or player salaries. Just look at the how much the Wilpons made when Selling the Mets to Cohen. This is why I’m in favor of raising league minimums and a pre-arb/arb/FA structure that gets more players into arb a year earlier or into FA a year earlier. This will help the average player a lot, and have no effect on the mega-stars like Harper, Cole, Scherzer,

Mookie, etc. Owners will resist this though as it’s about making MORE $ in everything they do!

Yes, but the valuation is only a paper number until they sell. What determines payroll is revenue. Of course the owners are rich. They couldn’t afford the team otherwise. But their bank account in 99% of situations, is not part of that revenue stream. Its separate, and has nothing to do with payroll. The same people who say a $20MM tax should not stop a team from spending, are probably people who won’t buy online if there is a shipping fee. Its different when its your money.

@ giantsphan12

No, the reason the owners won’t ever go for reducing years of control is it hurts the small-markets/mid-markets way to much. No idea why this is so hard to understand? It’s almost as if you’ve never thought of this as a possibility being a giants fan and all.

Not all, but most fans of large-market teams are clueless to the realities of 60+% of the big-league teams around the game. The eyes just keep a rolling with each and every ignorant large-market teams fans thought-pattern on the subject of baseball.

While this is true, it’s also true that the owners could solve the big-small market problem by sharing more of the game’s revenue to the point where team resources are a lot more balanced than they are now. If they did that, the CBT becomes unnecessary, and reducing team control years becomes realistic. As many problems as this would solve, it hasn’t happened, and it isn’t going to happen. The big-market teams are only going to share so much of their riches.

@ BlueSkies

That’s been my mantra since the first $200MM a year local TV contract came to being more than a decade ago. My user name more than 2 decades ago, sold the majority of large-market owners that revenue needed shared for the good of the game, the lack of competitive balance was destroying the game. Instituting RS restored competitive balance until the large-market local TV deals exploded upward.

Today we have revenue gaps larger than at any time in baseball history. And no more Bud Selig or anyone like him that’s able to galvanize the number of owners needed to ok an increase in revenue-sharing that is needed to restore competitive balance to the game.

So you are correct sir with your take, and unfortunately I agree with you in that it’s not likely to change, at least anytime soon.

Seems to me the broken media model drives the revenue inequities. When the Dodgers were sold a lot of people thought Guggenheim was nuts to pay over $2B for the team, but hardly anyone then appreciated that the team’s old media deal was about to expire and the new one would be worth many billions (and would be sweetened further by the bankruptcy court). Teams in smaller markets especially if they are stuck in the middle of a less lucrative media contract are hamstrung. It’s all based on accidents of timing and where the teams play their home games. It’s a crazy system but seemingly nobody has any appetite to fix it. Even the small-mid-market team owners apparently don’t. They’re getting enough revenue sharing to keep them happy, which tells us something.

Yeah in a way but ask the previous owner of the Rangers who went belly up and Nolan Ryan group bought it out of bankruptcy. Profits aren’t a guarantee. That’s why small markets don’t act like big markets.

If you’re saying it isn’t impossible to run a good business into the ground through mismanagement, sure. That’s what McCourt did to the Dodgers, and for his sins was turned into a billionaire a couple times over. Failure may not be impossible in this business, but they make it pretty difficult.

Feels like the strike nearly 30 years ago. Players and owners refusal to engage and having the season wasted away. It took a year and a half to settle on something 30 years ago. If it goes like last time, it will ruin baseball for good. Fans like myself, lived through it that one and came back a few years after. If it happens again as it is currently going, it will be hard for me to come back this time around. It’s a stalemate like back in 93-94.

Shhh****tttt. What would you watch then?

I don’t care if they lose the whole season in the middle of another variant canceling bowl games and pausing seasons.

Personally I don’t think they’ll miss a single game until later in the year when omnicron or some new variant wipes out a whole pitching staff. But I think a HR derby to determine who wins the game could be a fun alternative.

My sentiments exactly!

You stated this perfectly!

The high revenue teams are basically treating the CBT as a form of a cap. They go over, but then they they pull back under. The “Yankee tax”, as it was originally called, has worked, as their payroll has basically flat lined over the past 15 years, even as revenues across MLB, and certainly the Yankees, have skyrocketed. Son of George was even on board with lowering the tax threshold to $180M, although he may have said that knowing it was never going to happen.

The MLBPA should hold firm and demand a significant increase. The owners will cave simply because increasing the tax threshold doesn’t actually cost them anything. The harder they fight raising it will be confirmation they’ve implemented a form of a cap.

Get out of here Manfred. The revenues would increase without a luxury tax. You’re ruining baseball Rob. Just make it like the NFL with salary’s caps that no one understands and teams can always circumvent

Wondering if taxing teams on AAV and/or ticket prices would work?…

It would definitely work

The owners would never go for this because they would have to open their books

Solid idea tho.

A lot of fans can’t afford ticket prices and concessions. Logically, more fans means more money so maybe there’s a way to convince the owners. Just a thought

The luxury tax revenues should go to help the minor leagues not to teams that don’t spend it anyway.

@kingman

You mean don’t spend it on payroll. Some teams may be using it to support their minor league systems, but that doesn’t get reported publicly. They could be using it to pay off debt on the stadium, or debt that was acquired when revenue sharing was suspended. There are no requirements that the RS has to be applied to payroll. If the RS keeps small market teams afloat during hard times (due to economy, pandemic or failure to draw) its serving its purpose to keep teams throughout the country.

They need to decrease the threshold! These contracts need to be tamed back you have players making 40 mil a year that is bonkers, take a team like Tampa that barely spends 80mil a year that’s half their TEAM payroll! Hold firm MLB.

Or how about the billionaire owner of the Rays ups his team’s payroll and gets them out of that terrible field. Imagine if the rays spent over a 100 million on their team with their ability to develop players.

Not a billionaire if your net worth is under a billion. Per yesterday’s MLBTR article:

Rays: Stuart Sternberg – $800MM.

The luxury tax just puts more money in owners’ pockets. It won’t reduce ticket or concession prices.

Theae guys should be locked in a room with no air circulation? only water- no food. And don’t come out til you come to an agreement.

@coop, see my post 2+ weeks ago.

“After a big bbq with baked beans, deviled eggs and all the fixins; lock the owner and player negotiators in a room with no bathroom facilities”. 2 hours max, done deal.

Add hot Cheetos and you got it

The CBT was always supposed to act as a soft salary cap, and that is exactly how teams have been treating it. So no one should be surprised by this or surprised by the fact teams will be reluctant to exceed it year after year. It was an attempt to address the fact that there are significant financial inequalities between the richest and poorest franchises in baseball and attempt to control the spending of the richest.

Has it worked? Yes, and no. Yes, because some of the highest spending teams have reigned in their spending at times to get under the threshold. No, because the serious financial inequalities between franchises still exist. The poorest teams cannot even come close to spending with the richest teams. So they have to find a way to try to field competitive teams from time to time. That has lead many teams to trade off their veteran talent and try to develop a core of young, controllable players they can develop as a group and hope they become the core of a competitive team before they lose control of them. Because that leads to a lot of losing early in the process, it has been referred to as tanking. It is not, because it is a legitimate business strategy to forgo short term gains for a better longer term gain. It is not always successful but like any plan, it won’t work unless it is executed correctly.

Now this strategy is not new, but the reason it is an issue is the volume of teams going through it at the same time, which lead to a reduction in mean and median salary for players, largely because a lot of mid to low tier veterans went wanting for jobs because of this. But this is largely cyclical and already several of the teams that were in that mode are signaling they are coming out of that mode. So had the current CBA expired a year later we likely would have seen an increase in mean/median salary for 2022. Likely still will see that even with a new CBA.

Raising the CBT significantly will only lead to more teams entering a rebuilding phase, not fewer, which could very well suppress mean, median salaries. MLBPA would serve their membership much better by agreeing to modest CBT increases in exchange for significant elevation of the minimum salary. Teams will still go through rebuilding phases, but that young talent will cost them more and could lead them, and other teams to reconsider those mid and lower level veterans as it will likely tip the cost benefit ratio towards those veterans.

Waiting for the comments about “evil rich people” arguing over money.

I don’t find rich people evil at all, only when their money gets in the way of proper thinking are they loathsome.

I like rich people. I’ve never worked for a poor person. Baseball would be awful if owners were poor. But there is lots of wealth envy on here so waiting for it to show up in the comments.

I’m pretty sure that rich people don’t care or like you….in fact they despise you

You have no clue.

prov356

I like rich people.

===========================

I get paid semi-decently for helping rich companies to produce reliable financial statements. And they’ve contributed to both my defined benefit and defined contributions pensions.

And they sell me cars, TVs, phones, etc. I like having rich people around.

Tax those below 100M and over 200M. Even it up and get on with it.

^ this

If you tax a team that currently cannot afford a $100MM payroll, where do you think that tax money will come from? Hmmm…, what part of business expenses has flexibility? Taxes? no. Building/stadium costs? No. Payments on debt? No? Travel? No.(union agreement won’t allow coach, or motel 6). Marketing? Yep! Only so much can come out of marketing, and making it more difficult for a team to sell their product, doesn’t help the players or the team. Payroll for staff? Yep! But cutting the number of coaches is a minor savings, and cutting the analytics dept puts teams at a disadvantage, and curtails the development of the players. That leaves player payroll to cover the cost of that payroll tax. Brilliant idea. Lets have Pittsburgh, Cleveland, and Florida drop payroll even lower to cover the tax.

$100M is definitely unaffordable ?

Not sure. 100m is just a guess at a doable number. If you structured the tax appropriately, you couldn’t make ramping up the payroll to 100m the least expensive option ?

Yeah in a way you are correct but ask the previous owner of the Rangers who went belly up and Nolan Ryan group bought it out of bankruptcy. Profits aren’t a guarantee. That’s why small markets don’t act like big markets.

Stop wasting our time and play the game.

Start the CBT @ $215M and raise it $5M per year, provided that league revenues grow year over year. If they have a season of flat revenue or a reduction, then the CBT remains the same as the prior season. This way, the owners would at least tie something in the CBA to total revenues as the union has been asking for. The owners might not like to set that precedence though.

That’s only a 2% annual increase in an industry with annual revenue, salary, and franchise values typically increasing at a much higher rate. Increase the CBT by $20-$40M for 2022 and then 5% per year.

Maybe the tax shouldn’t escalate each year a team is over. Make the penalty 20, 25 or 30 percent no matter how many years a team exceeded the threshold. Teams wouldn’t need to dip under to reset the bracket. And if the tax was just a few million, which it usually is in the first year, teams might be encouraged to not worry about it. But, a team that far exceeded the threshold would still take a significant financial hit.

Season tickets sales must suffer with the lockout. I wouldn’t buy one without assurance a full season will occur. The owners are playing a risky delay game. No baseball news means reduced interest. Reduced interest means reduced income.

Agreed. I’d love to see some stats on how teams have done so far with both renewing season tickets and selling new season tickets. Most teams do a holiday push for season ticket sales; I’m willing to bet that was an absolute flop this year. The real telltale sign will be how many people chose not to renew. If owners are seeing a 10-20% decrease in renewals then that will really open their eyes and force them to come to an agreement sooner than later.

The biggest issue with the repeater tax is not necessarily the money owed but it is the draft pick penalties, including lowering of your draft pick by 10 spots, the loss of International Free Agency funds and the penalties associated with signing a free agent who was given a Qualifying Offer if that team went over the CBT in the previous season. Even the richest teams know the importance of the draft and how developing young players with low salaries is crucial to sustaining a winning ball club. The draft is already a crap shoot but if you lose draft picks or lose IFA money, you are at a competitive disadvantage that will eventually catch up to you. If they did away with the draft pick / IFA penalties, we’d see a lot more teams willing to exceed the CBT year over year.

There also needs to be a salary floor – Teams must have a minimum player payroll as a function of their revenue. For instance despite the pandemic, the Baltimore Orioles had 2020 revenue of $115M yet their 2022 payroll will be under $25M.

I would also like to see a penalty for finishing in the bottom 5 for regular season for more than three or more years. Either a monetary penalty or draft pick penalty so an organization can’t hoard all the top talent.

Seeing as how there is an MLBPA, it’d be nice if there was an MLBFA – an MLB Fan’s Association. But how would we as fans determine who represents us?

I understand that fans feel neglected in this process, but why do we deserve a seat at the table? Do car owners expect to be represented when GM or Ford is negotiating with the auto union?

I see where you are going with this comparison but I don’t believe the two are congruent.

Sports and it’s athletes are more tangible than what goes on in and behind the assembly line for vehicles. There isn’t a section in the paper devoted to how many cars a GM plant churned out in a week vs how many they sold compared to competitors.

Members of the UAW produce a product that the majority of us use. No one watches them make these vehicles and we don’t pay to see them perform their job. The everyday driver doesn’t want or need to be in the negotiation room between union and company but they do want their ideas/needs heard in the subsequent iterations of car models. This typically happens when companies look at end of the year sales as where consumers put their cash is a decent indicator of why they like or dislike certain cars.

In sports, athletes are the product. We go to games to watch them perform. The dollars spent to attend a game are (or should be) partially used to put a competitive team on the field. If season ticket holders or a family of four routinely go to games only to see the home team continually cellar dwell, where is that money they’ve worked hard to make going in terms of on-field investment?

Having an MLBFA is a transient and fuzzy idea, but I do think a payroll floor is necessary.

It sounds like a minimum spending floor per team is not a viable option, but there should be some sort of penalty for teams that don’t spend enough on payroll. Perhaps they could limit the amount of revenue share they receive. For example, a team doesn’t get any revenue share for payrolls under $50M; they only get 50% if they spend under $65M, etc. Also, the draft order needs to be changed to an unweighted lottery for the bottom 8-10 teams (each would have the same chance of getting the #1 pick). Something needs to be done about these teams that refuse to spend and purposely field a non-competitive team.

This is a great way to change the fan base and markets for the nonspenders. Miami, Tampa, Pittsburgh, Oakland. And Cincy appears to be in sell-mode. Oakland and Tampa are competitive but their ownership sucks. The revenue needs to improve the foundation of those teams and if ownership won’t do it, then find someone who’ll spend or relocate. There’s too much money made in baseball to not improve the sport as well as the minors. To expand the sport, we have to stop seeing guys rather play elsewhere than MLB due to $. I don’t believe you have that problem in the other 3 major sports; where the teams can’t afford a guy so they leave the league. I’m mainly referring to the players in Japan.

How are Tampa and Oakland bad if they are able to compete at low payroll? Sounds like a great ownership/ management and explains why other teams pilfer their staff. Want to see equality? Have MLB act like a real franchise operation. Reassign the management every five years. Would love to see what Tampa mgt could do with LAA. It would be even more fun to watch Cashman in PIT, or Dombrowski in CIN. Don’t want to see the management get stale in their jobs!

Doing a draw for draft picks makes much more sense in NBA and NHL where there is a salary cap and revenue sharing. With the unequal floor in MLB, small market teams have the hurdle of getting a lower pick when they succeed. Tampa Bay picking 26th hurts more than the NYY picking 26th, as Tampa Bay doesn’t have the option of signing Cole, or Correa in FA. What it does is makes them more likely to rebuild when the farm is thin. Removing the only realistic option of a small market competing because their Top picks didnt develop as expected (the rarity being a first rd pick living up to the billing) is rather absurd. It took the Cubs 100 yrs to put things together, and they are not a small market.

The idea of the tax was to holding spending and to send the tax funds to the clubs with lower payrolls. The pirates and another team received the tax money but never put it back into the team, just in their pockets, so the mlbpa should require that the tax go back to payroll

The reason the CBT was instituted was not to hold down spending, though that is a result, but to try and maintain a better competitive balance between the big and small market teams. The league wanted to prevent the big market teams from unlimited spending, and out-bidding the small market teams for FA players.

The NFL hard cap was instituted for the same reason. But since that was something the MLBPA would never accept, the CBT was the compromise. For that reason it isn’t going away. Now whether they can agree to the necessary modifications to the CBT is another thing.

@citizen

There is no requirement to put the revenue sharing to payroll. That you don’t see where it was put, doesn’t show it was put in their pockets. Teams have other expenses to cover, not just player salaries.

The league’s salary cap proposal is not a serious offer. The salary cap in the NFL and NBA is tied to a floor and a guaranteed percentage of revenue close to 50%. The floor is about 90% of the cap, meaning teams have to spend close to the same amount of money (the NFL does this over 4 year periods, the NBA does this yearly). MLB’s proposal offers neither of these things. A $100m floor with a luxury cap at 180 is still allowing massive gaps between teams in spending, and still guarantees the players even less of a percentage of the pie.

In 2019, the player salaries made up less than 40% of the league’s revenue. That’s considerably lower than the NFL or NBA. If they had an NBA style cap at 50% of revenue, that cap would be at about $178m, with a floor of 160. Of course MLB would never agree to something like that. Because it would mean having to redistribute the revenue, and they don’t want to do that.

Factor in the manipulation towards free agency and that is a big reason why MLB is behind the other major sports. not only is the less pie when you get paid, you have to wait to get paid if you last that long.

@ chest bridge

Could be that the larger costs of a longer season don’t allow the same flexibility for payroll that a 16 game NFL season, or an 80 some NBA season provide. I also would like to know where you’re getting your numbers from, since only Atlanta has public numbers available. It may very well be accurate, but knowing your source would provide more confidence in them. Without that source, it simply appears to be conjecture on your part. (I don’t believe everything I see on the Internet.)

130 floor, 160 ceiling. Salaries would jump up quite a bit compared to the recent norms probably but it should be in the ballpark.

250/200, raised to those levels over the next five years. Some revenue sharing will need to be adjusted. The thresholds should be indexed yearly.

Teams that can’t handle those thresholds can opt to pay significant penalties, with the money split going equally to MLB and MLBPA; or make preparations to move to new markets or new stadiums; or sell to wealthier owners who are committed to fielding winning teams. Let the good times roll.

Moving a small market team to an even smaller market is really your solution @lord99?

thank you for the update

It’s pretty easy to summarize ownership’s position on the CBT:

“Stop us before we spend again!!”

No point in being frustrated. The two sides weren’t going to get a new deal done before the New Year much less negotiate since they’ve all probably been on holiday mode. Enjoy the holidays with your favorite people and hopefully the new CBA is established without any regular season games being compromised.

I think neither side is motivated to create the best version of the game. They just want to fight over money. I get it, but I wish there was interest in growing the game. I think MLB is poor at this.

The reality is that the game is becoming less watchable and more and more people consume the game in highlights, replays, and app updates.

Yet the players doesn’t want a salary cap, but the big market teams are using the luxury as a hard cap.

Not only do the players not want a salary cap, they’ll never accept one. If there is one deal-breaker for the players it’s the salary cap.

The big market teams may be using the CBT as a hard cap, but that’s only because the big market are the only teams up against it. The big market teams wouldn’t mind the CBT going away.

Most teams (over half) don’t plan their payroll around the CBT as their revenue doesn’t allow it. BAL, TB, CLE, CHW, DET, MIN, KC, OAK, SEA, ATL, MIA, MIL, CIN, PIT, COL, and ARZ won’t be spending more because the CBT changes. Probably true for a few others like CHC and STL as well. It simply tries to keep the big markets in check. Other than LAD, it seems to be doing that. Raising the amount will suck for fans of the above teams as it will make it harder to compete with the big boys, as long as their markets are protected by MLB.

I think all competitive taxes should be paid out to charitable organizations that fit a mold of 95% funding to actual need on the charity. Fans vote for the charities 2 times a year. Charities audits on where funds were spent.

How did the cubs exceed the tax threshold in 2020? They didn’t spend any money?

Raise the cap but make it a HARD cap. None of this circumvention because for the richest teams, the threshold doesn’t matter.

Also create a hard floor at 2/3 or 70% of the cap figure. There are 10 teams immediately better for having to do this.