NL East Notes: Mets’ Payroll/Rotation, Nationals, Marlins

Mets GM Sandy Alderson said at yesterday’s Yoenis Cespedes press conference that the significant signing illustrates that the team is working without payroll limitations, as MLB.com’s Anthony DiComo writes. Alderson was asked if it’s possible that he can retain his entire rotation for the long haul, and while the GM unsurprisingly didn’t want to commit to anything, he did note that the increased payroll flexibility creates the possibility for some long-term deals. “I don’t want to foreclose any possibility,” said Alderson. “…I think maybe if the Cespedes signing says anything, it’s that there are no possibilities that will be dismissed out of hand strictly for financial reasons.” Alderson said the team will get a better feel for any mutual interest in extensions over the next several weeks as Spring Training looms and eventually kicks off. Of the team’s excellent rotation core, Matt Harvey is the only one that has already reached arbitration eligibility, although as a Scott Boras client, he’s perhaps an unlikely candidate to sign long-term in the first place. Next winter will see Jacob deGrom and Zack Wheeler reach arbitration. (MLBTR’s Jeff Todd and I discussed extensions — and not just for the Mets’ rotation — at length on today’s MLBTR Podcast, for those interested in the matter.) Perhaps most notable of all of Alderson’s payroll comments, however, is the fact that he said he doesn’t anticipate returning to the club’s previous payroll levels even if Cespedes opts out after this season. New York’s payroll will be in the $140MM vicinity for the 2016 season.

Here’s more from the NL East…

- Every contract the Nationals offered to a free agent this winter contained significant deferrals due to uncertainty over the team’s MASN television dispute, writes Barry Svrluga of the Washington Post. The issue came to light most prominently after the team’s failed pursuit of Cespedes. While the Nats technically offered $110MM over five years, Svrluga spoke to sources on both sides of the negotiation who felt the Mets’ offer was clearly better. As he notes, there’s perhaps no need to look further than the first year of the deal; Cespedes landed a $10MM signing bonus and a $17.5MM salary for the 2016 season — $27.5MM up front, with the possibility to max out at $75MM over three years — but would’ve received just $7MM in 2016 with the Nationals’ offer, which contained a decade’s worth of deferrals. One person that spoke to Svrluga called the team’s $200MM offer to Jason Heyward “the most complicated deferral” that person has ever encountered, noting that it contained 16 years worth of deferred monies. Even the players they’ve managed to sign over the past two years — Max Scherzer and Daniel Murphy — come with notable deferrals. Svrluga points out that Scherzer will be owed $15MM in the first year after his deal ends, and while delaying that payment drives down the value of those funds, Svrluga is correct to note that said line item on the team’s budget could interfere with the Nats’ ability to add some secondary pieces six years down the line.

- The Marlins continue to search for veteran rotation options, but president of baseball operations Michael Hill has very little to work with remaining in the budget that was given to him by owner Jeffrey Loria, Barry Jackson of the Miami Herald writes. Jackson notes many of the same names that he and Jon Heyman connected to the Marlins a couple of weeks ago: Kyle Lohse, Tim Lincecum, Alfredo Simon and Cliff Lee (though based on the picture Jackson painted in referencing the tight budget, Lee seems somewhat unlikely).

Details On The Nationals’ Offer To Yoenis Cespedes

Prior to the Mets’ re-signing of Yoenis Cespedes to a three-year, $75MM contract with an opt-out clause after the first season, the Nationals were viewed as the primary competitor for his services, offering a reported five-year deal with a value said to be around $100MM and an opt-out after two years. A pair of reports from Jon Heyman (Twitter link) and Peter Gammons of the MLB Network (at GammonsDaily.com) now shed some further light on the matter. According to Heyman, the base value of the contract was $110MM, but the deal contained “significant” deferrals. While that info alone makes it difficult to compare the two offers, Gammons adds further context, stating that the $110MM was to be paid out over a 15-year term, and after factoring in the deferred monies, the present-day value of the proposed contract was roughly $77MM.

If that number is indeed accurate, it’s not surprising to see that Cespedes chose a comparable amount over a shorter contract that contained an earlier opt-out date with a team/city with which he was already familiar. Of course, it should also be noted that the present-day value of any multi-year contract is somewhat less than the face value of the deal; the $47.5MM that Cespedes would earn from the Mets if he does not exercise the opt-out clause will be worth less in 2017-18 than it would be in the present day. Nevertheless, the extent of the deferrals in the contract proposed by the Nationals certainly appears to make the Mets’ offer a stronger option, barring further revelations about the pair of proposals.

As Gammons continues, the Nationals had to offer significant deferrals not only to Cespedes, but also to Jason Heyward and Ben Zobrist in their respective pursuits, due largely to the structuring of the MASN television contract. Because of the deferred money in their offers to Heyward and Zobrist, neither proposed contract was even close to the overall value that the duo got when ultimately signing with the Cubs. In Heyward’s case, the Cardinals’ offer was also significantly stronger than the reported 10-year, $200MM contract proposed by the Nats, after factoring in deferrals, Gammons notes.

Per Gammons, the structuring of the MASN television rights required the Nats to offer significant deferrals in virtually all of their contract offers this winter. Back in November a New York Supreme Court Judge ruled in favor of the Orioles (the majority owners of MASN), thereby voiding a payment of tens of millions of dollars that had been awarded to the Nationals by an arbitration panel in an effort to settle an ongoing dispute over the allocation of the network’s rights fees. (MLBTR’s Jeff Todd examined the dispute at length at the time of the ruling.) As Gammons notes, the difficulties for the Nationals will continue to linger until the two teams can come to some type of resolution on the matter.

The Dollar Value Of Recent Opt-Out Clauses

Following a wave of multi-year club options attached to deals, players and their agents have begun to request and receive player options in recent years as well. David Price, Johnny Cueto, and Jason Heyward have each received them this winter, meaning that quantification of such deals is essential for careful team building. (Editor’s note: this article was written before the Dodgers reached an agreement with Scott Kazmir.) Everyone up to the commissioner has expressed concern that these “opt-out” clauses have been included in deals, and some feel teams simply should not give them. However, this is akin to saying that teams should not pay players above the league minimum salary—of course teams would like to do this, but you need to give players compensation to sign them. An opt-out is a way to lower the cost in dollars to the team, because the player will want more money otherwise.

Each of these three deals would be substantially more expensive without opt-out provisions—each opt-out clause is worth around $20MM, by my calculations. To test this, I looked at how a rough weighting of previous years’ WAR would affect a future projection, and compared this to how that projection would crystalize as it got closer. This led to an estimate that a very rough projection of future value 2-3 years in advance would change by about 1.0 WAR over the following 2-3 years. A more sophisticated system would probably change by about 0.7 WAR as it gets closer—and dollar value would probably change by about $7MM per year after accounting for overall uncertainty in salary levels. (The relationship between dollars and WAR utilized in this post is explained at this link.)

Given that potential level of variation, there are still a wide band of possibilities in terms of what a given player’s expected future value will be at the point of decision on an opt-out. But at base, an opt out is a binary choice: yes or no. Based on what we know now, and based on reasonable projections, we can estimate a given player’s future expected value at that point of decision by weighting different possible outcomes.

In other words, if Player X opts out, we can assume it is because his anticipated value at the point of that decision is higher than that which he would have earned through the remaining portion of the contract. But we don’t know exactly how much higher. So, to arrive at a value for the scenario in which a player does opt out, I’ve weighted all of those possibilities and reduced them to a single dollar value. The same holds true of the situations in which the player does not opt out.

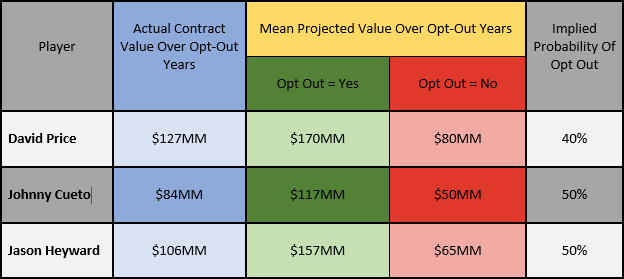

We’ll get into each player’s situation further below, but this table shows the results of the exercise. (App users can click on this link to see the table image.)

David Price received a contract for seven years at $217MM, but it was really a three-year contract for $90MM with a player option of four years and $127MM. If Price only held teams to a three-year commitment, he would probably get close to $120MM—but this is not what he did. Instead, he will require $127MM for 2019-22, only on the condition that he looks to be worth less than that by then. Although $127MM is not a terrible estimate of his 2019-22 production as of January 2016, this value will probably change drastically by October 2018, one way or the other. If he does not opt out, he probably will have performed worse, and conditional on the assumption that he will not have opted out, I estimate his expected value for his 2019-22 seasons to be $80MM. If he does opt out, he probably will have performed better, and conditional on the assumption that he will have opted out, I estimate his expected value for those seasons to be $170MM. Given that this corresponds to roughly a 40% chance of opting out, his opt-out clause is worth about $17MM, meaning that his seven-year $217MM contract is roughly equivalent to a seven-year $234MM contract with no opt-out clause.

Johnny Cueto’s contract is somewhat trickier, but it essentially amounts to a deal of two years for $46MM, with a player option of four years and $84MM, followed by a club option of one year for $16MM. Cueto would probably be worth $17MM above his salary for 2016-17. But for 2018-21, he is likely to be worth $50MM if he does not opt out and $117MM if he does. With roughly even odds of opting out, this makes his opt-out worth about $17MM. While the club option for 2022 makes the deal somewhat more attractive for the Giants, the odds that he will be worth much more than this are low. Overall, Cueto’s six-year deal for $130MM would probably cost about $147MM with no opt-out clause.

Jason Heyward’s contract is even trickier, but it mostly boils down to a three-year deal for $78MM, followed by a five-year player option for $106MM—except that the first player option (if exercised) is only certain to include one more year for $20MM. That’s because there’s a vesting provision that, if triggered—by Heyward reaching 550 plate appearances in the season following the initial option decision—would give him yet another player option for four years and $86MM. (If he exercises the initial option but then doesn’t reach that PA threshold, then both sides would be stuck with the remaining four years of the contract.) Heyward’s value is further complicated by the fact that signing him required forfeiting a draft pick, which is worth around $9MM.

Although Heyward’s contract contains two opt-outs, it is not all that likely that he opts out after 2019 if he does not after 2018. Players’ values do change substantially, but he is likely to be either much more valuable than his five-year player option after 2018, or much less valuable. It is not that we expect his value to look similar after 2018 and 2019—it is that he will probably already be way above or way below the current expected value near $20MM per year, and is likely to remain way above or way below this line through 2019.

For the first three years of Heyward’s contract, I estimate that he is worth about $22MM more than his contract will pay him. With five years of player option, there is a wide range of potential values afterward. I estimate that he also has about even odds of opting out, but if he does not opt out then he is probably only worth $65MM, while if he does he would be worth $157MM. If he doesn’t opt out after 2018 and does after 2019, he is likely near the middle and the value of the second opt-out is small. The net effect is that his opt-out clauses are worth about $25MM, and he would probably have received $209MM for eight years instead of $184MM had no opt-out been included in the deal.

With values of $17MM for each of the two pitchers and $25MM for Heyward’s pair of opt-outs, these opt-outs help keep costs down for teams. While they contain more downside and less upside than typical free agent contracts, they cost less money as well. As teams move forward in this new market, they should be careful to properly consider the true cost of these player options. If teams are willing to expose themselves to some downside risk, they can lower the cost of acquiring elite players.

NL Central Notes: Heyward, Cubs, Cardinals, McCutchen

Jason Heyward says one reason he chose the Cubs over the Cardinals is that the Cubs’ young core is likely to be with the team longer than the Cardinals’ core is. “You have Yadier (Molina), who is going to be done in two years maybe. You have Matt Holliday, who is probably going to be done soon,” Heyward told reporters, including Paul Sullivan of the Chicago Tribune. “I felt like if I was to look up in three years and see a completely different team, that would kind of be difficult.” Cardinals manager Mike Matheny says he believes in the core of his team and takes issue with Heyward’s comments, Rick Hummel of the St. Louis Post-Dispatch reports. “I don’t blame him. But I don’t like it,” says Matheny. “I don’t think we have anything to apologize for in having a group like a Holliday, a Molina, a Wainwright. … [H]e’s a young player. But I can’t say I’m in any kind of agreement with that (Chicago) core being better than any kind of core that we have.” Here’s more from the NL Central.

- Elsewhere in Hummel’s article, Cards GM John Mozeliak expresses a bit of frustration that the Cardinals’ biggest offseason targets — presumably players like Heyward and David Price — opted to head elsewhere. “Our success has really come from our pipeline, and I think we’re really going to lean on that. The last month has been trying to play in the big-boy pool, and unfortunately we just didn’t end up getting it done,” says Mozeliak. “Sometimes it’s not always about what you’re doing. You need the other party to want to be there, too.”

- Jason Heyward’s mammoth deal with the Cubs got some reporters, including Bill Brink of the Pittsburgh Post-Gazette, wondering how much it might cost a club to sign Pirates outfielder Andrew McCutchen if he reaches the open market after the 2018 season. For his part, McCutchen doesn’t want to speculate on his own dollar value, but he did reaffirm his loyalty to Pittsburgh. “This is still a place I do want to be,” McCutchen said. “I love it here. If that’s something that they can do, that’s something they can do. I really can’t answer from their end. We’ll see what happens in the future.” Of course, as Brink points out, Heyward in 2015 and McCutchen in 2018 are two separate cases. Heyward got his monster contract, in part, because he is only 26 years of age. Following the 2018 season, McCutchen will be 32.

Zach Links contributed to this post.

Cubs Notes: Price, Bullpen, Heyward

The Cubs made a run at David Price this winter, but they weren’t necessarily close to landing him. Chicago fell roughly $50MM short of the Red Sox’s offer, Cubs president of baseball operations Theo Epstein told WEEI this week. “We ended up a distant third,” Epstein said.

“He’s a great pitcher and we were involved and very interested,” said Epstein, who was apparently also behind the Cardinals in the Price sweepstakes. “We thought, he’s an elite, elite pitcher, the kind that very rarely makes it to the free agent market, he’s got terrific makeup, where he influences a team not just through his performance on the field, but he’s a real culture-changer or a culture-enhancer, at the very least, in the clubhouse.”

Here’s more on the Cubs:

- The Cubs’ current focus is on trading for relievers, major league sources tell Ken Rosenthal of FOX Sports. Chicago isn’t looking for high-end types like Andrew Miller of the Yankees, but they are fishing for middle-inning and setup options who would provide additional depth. In the outfield, he adds, the Cubs’ plan is to play Jason Heyward in center field rather than add a center fielder and slide Heyward into right field. The Cubs could also consider a trade for a starting pitcher.

- After sitting on lower payroll numbers for six years, Cubs ownership has opened up the purse strings, Bruce Levine of CBS Chicago writes. Epstein & Co. now have a projected $155MM payroll on the 25-man roster for 2016, eclipsing the previous watermark of $145MM in 2010. The payroll should keep rising from here, thanks to a projected attendance hike this season and a TV contract that will give the Cubs billions of dollars worth of revenue.

- In his introductory press conference this week, Heyward explained that he was drawn to the Cubs in part because of the roster stability he expects them to have going forward. “Knowing the core is young and those guys are going to be around for a while is very exciting,” Heyward said, according to Jesse Rogers of ESPN.com. “I don’t want to take the highest dollar amount when my gut is telling me to go somewhere else. Being 26 years old and knowing that my contract would put me in any clubhouse for longer than most people there, you have to look at age, how fast the team is changing and how soon those changes will come about.”

AL West Notes: Angels, Cespedes, Upton

Here’s tonight’s look at the AL West:

- Angels owner Arte Moreno said the Halos didn’t make any serious offers to any of the big free agents out there this winter, Jeff Fletcher of the OC Register tweets. More specifically, Moreno indicated that Angels did not make an offer to Jason Heyward and that the club is not in serious talks with Yoenis Cespedes, Justin Upton, Alex Gordon, or Chris Davis (Twitter link via Mike DiGiovanna of the L.A. Times)

- Angels GM Billy Eppler told reporters, including Mike DiGiovanna of the Los Angeles Times (on Twitter), that the team is still “engaged in conversations” with other outfielders even after the signing of Daniel Nava. Nava, it appears, is being counted on to provide the Halos with depth in left field, right field, and at first base. For his part, Eppler feels that there are still going to be opportunities to improve the club, even without the addition of marquee names, Fletcher tweets.

- Susan Slusser of the San Francisco Chronicle (on Twitter) gets the impression that the A’s were among those willing to bid more on Bartolo Colon than the Mets did. On Wednesday, Colon and the Mets agreed to a one-year, $7.25MM deal and he reportedly received more lucrative offers elsewhere. Colon enjoyed great success in Oakland, pitching to a 2.99 ERA with 5.5 K/9 and 1.4 BB/9 between 2012 and 2013.

Cubs Sign Jason Heyward

3:43pm: Heyward receives full no-trade protection from 2016-18 and limited no-trade protection in 2019-20, tweets Jon Heyman of CBS Sports. (Heyward will have 10-and-5 rights after that point, assuming he remains with the Cubs.) Heyman also reports that Heyward receives a $20MM signing bonus that is fully deferred, adding that the he’ll earn $15MM in 2016, $21.5MM in 2017-18, $20MM in 2019, $21MM in 2020-21 and $22MM in 2022-23 (links to Twitter).

Heyward can opt out after the 2018 season, and, if he chooses not to do so, will trigger a second opt-out clause following the 2019 season by reaching 550 plate appearances in 2019, Heyman adds.

DECEMBER 15, 2:34pm: The Cubs have announced the signing and are introducing Heyward today.

DECEMBER 11, 2:29pm: FOX’s Ken Rosenthal tweets that Heyward can opt out after the third year or fourth year if he meets certain plate appearance thresholds.

1:47pm: Heyward’s contract does indeed contain the option to opt out early, reports MLB Network’s Peter Gammons (Twitter link). However, he can opt out not only once, but twice, per Gammons. ESPN Chicago’s Jesse Rogers reports (also on Twitter) that the first opt-out clause comes three years into the contract, meaning Heyward can hit the open market entering his age-29 season if he chooses.

1:35pm: Bob Nightengale of USA Today hears it’s an eight-year, $184MM deal for Heyward (Twitter link) — an annual value of $23MM.

1:04pm: Heyward’s contract guarantees him less than $185MM and is believed to be for eight years, reports Wittenmyer (Twitter link).

12:12pm: Jason Heyward has chosen to sign with the Cubs, multiple sources tell Gordon Wittenmyer of the Chicago Sun-Times (Twitter link). Exact financial terms aren’t known, but Jon Heyman of CBS Sports tweets that the Cubs landed Heyward for less than $200MM despite the fact that the Nationals are said to have offered around, or exactly $200MM. An opt-out clause in the contract would certainly make some sense, though reports haven’t indicated that to be the case just yet. Still, Heyward’s agent, Casey Close of Excel Sports Management, has previously negotiated such clauses for clients Clayton Kershaw, Zack Greinke and Masahiro Tanaka.

Heyward, 26, adds to an exciting class of free-agent additions for the Cubs this offseason (really, in the past week or so), as the team has already agreed to a four-year, $56MM pact with Ben Zobrist and a two-year, $32MM contract with John Lackey (to say nothing of a one-year deal to bring back Trevor Cahill, who had a relatively quiet resurgence in the Chicago bullpen).

Like Lackey, Heyward rejected a qualifying offer at the beginning of the offseason, meaning he’ll cost Chicago a draft pick. The Cubs, then, will be forfeiting the No. 28 pick in the draft as well as their second-round pick, which would’ve fallen in the early 70s when factoring in the first Competitive Balance Round and compensation picks for teams losing free agents that rejected the qualifying offer.

The question following this addition, of course, will be how Heyward slots into the outfield. The three-time Gold Glove winner is known as one of the game’s premier defensive players but has been almost exclusively a right fielder. Consensus seems to be that he can handle center field if need be, but with a pair of highly controllable assets flanking him in the form of Kyle Schwarber and Jorge Soler, it’s conceivable that the team will make a move to flip a young outfielder (Soler has been mentioned in rumors far more than his young counterpart, Schwarber) in order to further strengthen the rotation. Of course, that would again leave the Cubs with a hole in center field that needs to be addressed.

Defensive metrics are, of course, imperfect, but it’s still notable that since debuting in 2010, Heyward leads all Major Leaguers, at any position, with 119 Defensive Runs Saved. He’s also the runaway leader in cumulative Ultimate Zone Rating in that time (+94.4), and his prorated UZR/150 of +18.4 trails only Juan Lagares and Andrelton Simmons among qualified fielders. Those rankings hold weight even when shortening the sample size to the past three years, as each metric agrees that Heyward is the best defensive player in the game aside from his former Atlanta teammate, Simmons.

Wherever he fits onto the diamond or into the lineup, Heyward will strengthen the Cubs not only defensively but on offense as well. Though many point to his lack of home run power in recent years — he’s averaged 13 per season since 2013 — Heyward has continually whittled away at his strikeout rate and posted consistently strong on-base percentage marks (especially relative to the declining league average in that regard). In his lone season with the division-rival Cardinals, Heyward batted .293/.359/.439 with 13 homers and 23 steals (in 26 attempts). His offensive output was 16 percent better than that of a league-average hitter when adjusting for park, by measure of OPS+, while a similar metric, wRC+, rated his park-adjusted offense to be 21 percent better than the league average.

That the Cubs will effectively be signing Heyward away from the Cardinals only sweetens the deal for the club. Much in the way that the D-backs felt extra value by keeping Zack Greinke away from the Dodgers and Giants in signing him, Heyward will not only strengthen the Cubs — his departure will weaken one of their two biggest rivals. The same can be said of Lackey, who will also jump from St. Louis to the other side of the storied rivalry between the two franchises.

The Heyward market was quiet for a good portion of the offseason, but in recent days, the finalists were said to be the Cubs, Cardinals, Nationals and possibly the Angels, while the Giants also reportedly had interest but didn’t progress to the point of making an offer.

Photo courtesy of USA Today Sports Images.

Mozeliak: “Dynamic” Signing Unlikely For Cardinals

Having missed out on left-hander David Price and right fielder Jason Heyward, the Cardinals are unlikely to make a “dynamic” signing this offseason, GM John Mozeliak tells Derrick Goold of the St. Louis Post-Dispatch.

“It’s clear now this offseason is not going to have that dynamic signing that we tried to do with Price and Heyward,” Mozeliak explains. “There isn’t anything now that we’re chasing with a nine-figure contract. We can take the time to see what we have in the players we control. Obviously, we’re always open to adjusting.”

While that doesn’t eliminate the chance that the Cardinals could still add a notable free agent, it casts doubt on the likelihood of adding any of the top remaining bats on the market. Justin Upton, Yoenis Cespedes, Chris Davis and Alex Gordon — the latter two of whom have both been linked to St. Louis — all have cases to exceed $100MM on their next contracts. While USA Today’s Bob Nightengale said after Heyward’s agreement with the Cubs that the Cardinals would turn their focus to Gordon, Goold now writes that Mozeliak and his staff don’t consider Gordon an alternative to Heyward. Goold likens the scenario to the Price/Zack Greinke market, noting that the Cards didn’t jump into the mix for the latter upon seeing the former sign in Boston.

The Cardinals are still looking for upgrades to the pitching staff, whether in the form of an additional starting pitcher or a bullpen arm, writes Goold, though he notes that the market for starting pitching may need to change before St. Louis enters the fray for the top remaining names. The team has been linked to Mike Leake and Wei-Yin Chen, though Goold specifically notes that Leake’s market may have escalated beyond the Cardinals’ comfort zone.

Price and Heyward were considered to be exceptions to the Cardinals’ typically measured approach to free agency, according to Goold. Though the loss of Heyward stings more given the fact that he’ll head to a division rival, it doesn’t appear as though there was any lack of effort on the Cardinals’ behalf. Reports have already indicated that the Cardinals offered Heyward a larger overall guarantee, and Goold adds that St. Louis’ deal, too, included an opt-out clause. (Of course, Heyward’s agreement with the Cubs is said to contain two opt-out clauses and afford him a higher annual value.) Having been spurned by Heyward, St. Louis figures to enter the season with an outfield trio of Matt Holliday, Randal Grichuk and Stephen Piscotty (although Mozeliak said nothing to suggest that trade scenarios would not be entertained).

In the rotation, Adam Wainwright, Michael Wacha, Carlos Martinez and Jaime Garcia should all have spots locked down, while lefties Tyler Lyons and Marco Gonzales could factor in at the back end of the mix. Further additions shouldn’t be ruled out, although Goold does note that there’s a chance the only further signing would be to bring someone to camp to compete for a job in Spring Training. That, again, doesn’t necessarily preclude the Cards from upgrading via trade, though neither Mozeliak nor Goold indicated that said scenario is likely, either.

Reactions To Jason Heyward Signing With Cubs

Not only did the Cardinals lose out on Jason Heyward – they lost out while offering the most overall money, according to Derrick Goold of the Post-Dispatch. Two sources tell Goold that the Cardinals’ offer was greater in guaranteed value while the Cubs had the higher annual average value, at $23MM/year. As Goold notes, this marks the second time this winter that the Cardinals made a serious run at one of the winter’s top free agents and came up short. The other instance, of course, being their failed pursuit of David Price.

Here’s a roundup of reactions to Heyward’s massive new deal with the Cubs:

- The Cubs’ signing of Jason Heyward has left the Cardinals feeling jilted, Benjamin Hochman of the St. Louis Post-Dispatch writes. Now, the Cardinals must move on and add at least one significant piece, Hochman opines. The writer suggests that the Cards should sign Alex Gordon toplay right field or first base, with Stephen Piscotty playing the other.

- Ken Rosenthal of FOX Sports discussed Cubs president Theo Epstein, who now finds himself at the helm of baseball’s newest juggernaut. Within the article, Rosenthal writes that rival execs say Epstein has long been fixated on Heyward, going back to his early days with the Braves. Rosenthal also feels that the Cubs were motivated to sign Heyward and Lackey, in part, because they were effectively taking pieces away from the rival Cardinals.

- Things have changed in Chicago, as evidenced by the free agent additions of Heyward, Lackey, and Ben Zobrist, Patrick Mooney of CSNChicago.com writes. Back in November, Epstein says that he didn’t envision the Cubs being able to do two deals in the range of $100MM this offseason. Things quickly changed, however.

- The Cubs now have a monster lineup headlined by Heyward, Phil Rogers of MLB.com writes.

Cafardo On Bradley, Miley, Red Sox

A few teams, including the Royals and Cubs, inquired about Red Sox outfielder Jackie Bradley Jr. at the Winter Meetings only to be told that he was not available, according to Nick Cafardo of The Boston Globe. The 25-year-old Bradley (26 next April) posted a nice .249/.335/.489 bating line in 2015 and justified the considerable defensive hype that comes with his name, saving eight to 10 runs (based on his respective Defensive Runs Saved and Ultimate Zone Rating marks) while logging a combined 608 innings across all three outfield spots. It’s no surprise that he drew interest and also not a surprise to hear that the Red Sox are choosing to hang on to him.

Here’s more from today’s column:

- The Red Sox and Royals also discussed Wade Miley before he was shipped to the Mariners. A big league source tells Cafardo that Boston asked KC for Kelvin Herrera while the Royals preferred to move Luke Hochevar. The Red Sox ultimately opted for the Mariners deal. Miley’s first season with Boston got off to a slow start, but the lefty rebounded from a ghastly 8.62 April ERA to 4.10 ERA with a 137-to-58 K/BB ratio across his final 178 innings of the 2015 season.

- It “appears that” Cody Ross‘ career is over. The free agent outfielder suffered a bad hip injury with the D’Backs two years ago and he hasn’t been the same player since. The 34-year-old Ross was released by Arizona last season and later went 2-for-25 in nine games with the Athletics. Ross has played parts of 12 MLB seasons, suiting up for the Tigers, Dodgers, Reds, Marlins, Giants and Red Sox in addition to the Diamondbacks and Athletics, and hitting .262/.322/.445.

- Agent Joe Sambito tells Cafardo that free agent third baseman Will Middlebrooks has gotten inquiries from 11 teams. Cafardo speculates that the Brewers could bring Middlebrooks into their third base mix.

- Most execs and scouts that Cafardo spoke with at the Winter Meetings said that they wouldn’t give Jason Heyward a $200MM deal. Of course, the Cubs felt differently.