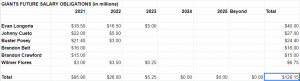

Giants Have Trimmed Long-Term Payroll Obligations

2020 salary terms still need to be sorted out. But what about what’s owed to players beyond that point? The near-term economic picture remains questionable at best. That’ll make teams all the more cautious with guaranteed future salaries.

Every organization has some amount of future cash committed to players, all of it done before the coronavirus pandemic swept the globe. There are several different ways to look at salaries; for instance, for purposes of calculating the luxury tax, the average annual value is the touchstone, with up-front bonuses spread over the life of the deal. For this exercise, we’ll focus on actual cash outlays that still have yet to be paid.

We’ll run through every team, with a big assist from the Cot’s Baseball Contracts database. Prior entries can be found here. Next up is the Giants:

*Includes buyouts on club options over Evan Longoria, Johnny Cueto, Buster Posey, and Wilmer Flores

*Reflects remaining portion of Evan Longoria salary owed by Rays

*Includes remaining signing bonus obligation to Johnny Cueto

(click to expand/view detail list)

The Slow Decline Of A Former Top-3 Pick

With the third overall pick in the 2014 draft, the Chicago White Sox selected Carlos Rodon out of North Carolina State. Rodon was a consideration for the top overall pick in the draft, but the Astros and Marlins each went with a high school arm in Brady Aiken and Tyler Kolek. As the top college arm in the draft, Rodon came with high expectations and a presupposed shorter timetable for reaching the majors.

Sure enough, it didn’t take Rodon long to reach the majors. He was the second-fastest from the draft class to make his debut, trailing only Brandon Finnegan of the Royals (debuted in September of 2014). Rodon made his debut in 2015, along with other top-10 draft picks from 2014 like Kyle Schwarber of the Cubs, Aaron Nola of the Phillies, and Michael Conforto of the Mets. Rodon came out of the gate hot, going 9-6 in 23 starts with a 3.75 ERA/3.87 FIP.

Rodon has now played parts of five professional seasons with the White Sox, but he has yet to put together a complete campaign. All in all, he’s largely been a disappointment. For his career, he’s 29-31 with a 4.08 ERA/4.25 ERA with 8.8 K/9 versus 3.9 BB/9 across 529 innings. Rodon’s numbers fit comfortably at the back end of a rotation, but the White Sox hoped for much more out of Rodon.

Rodon’s track record cannot be separated from his injury history. A sprained wrist in 2016, biceps bursitis in 2017, shoulder inflammation when he returned in 2017 that bled into the 2018 season, and then Tommy John surgery that ended his 2019 season after just 7 starts. It’s been a rough road since making his debut.

Entering 2020, the 27-year-old Rodon is a legitimate afterthought. He’s lost velocity over the years, with his four-seamer peaking early in his career with a 94.2 mph average and dropping to 91.4 mph over his seven starts of 2019. He’s gone away from the sinker that was his trademark early on, relying more and more on a fastball-slider mix that profiles more like the repertoire of a late-inning reliever. As he returns from Tommy John surgery, it’s hard to know what kind of pitcher Rodon will be.

Because of the delay to the 2020 season, however, he will be healthy and ready to go when/if the seasons starts, per Daryl Van Schouwen of the Chicago Sun-Times. That’s good news for Rodon and the White Sox, though it’s unclear if there’s room for Rodon in the rotation. Lucas Giolito and Dallas Keuchel are locked into the first two spots in the rotation. Gio Gonzalez was given a $5MM contract to do what Rodon hasn’t been able to: provide innings. For the other two rotation spots, Rodon will have to beat out a pair of young arms in Reynaldo Lopez and Dylan Cease.

Lopez, 26, has taken his turn every fifth day for the last two seasons in Chicago, but the results haven’t been tremendous (4.64 ERA/4.83 FIP) – and he’s just a year younger than Rodon. Cease, 24, made his debut last year and struggled, but he remains a promising, hard-throwing righty. They’re slotted into the rotation for now, but there’s never been more uncertainty heading into a season than we face in 2020. Rodon could very well push for a rotation slot, but his future is no longer guaranteed. Michael Kopech could also join the fray, as Van Schouwen notes that the former Red Sox farmhand should be recovered from his own Tommy John surgery.

The fact is, the rotation is the biggest question mark of the White Sox roster heading into 2020 – despite the high-ceiling potential therein. Given the bizarre circumstances of the current climate, the bigger question is how much rope Chicago will give their young arms. With a shortened season and expanded playoffs, the White Sox have increased expectations. Fans will expect the Southsiders to join the crowded playoff field. To that end, the early games will matter like never before. A guy returning from injury like Rodon won’t have the leeway to round himself into shape. What’s worse, he might not have minor league games to provide that extra runway either.

If Rodon can come back as effective as pre-surgery, he won’t be the ace that some imagined, but he can hang in a rotation. Whether he’ll get that opportunity in Chicago is unclear. Injuries take their toll, and Rodon has been through the wringer. Whether through side sessions or spring training 2.0, Rodon will have to prove he’s ready to contribute.

If the season takes place, Rodon will have just one more season of arbitration eligibility before reaching free agency, and the White Sox will have to decide whether it’s worth giving him a raise on the $4.45MM (full-scale rate) he’s due in 2020. Rodon is still young enough to turn things around in Chicago, but the injuries are piling up, and time is running out.

Pirates Have Minimal Post-2020 Payroll Commitments

2020 salary terms still need to be hammered out. But what about what’s owed to players beyond that point? The near-term economic picture remains questionable at best. That’ll make teams all the more cautious with guaranteed future salaries.

Every organization has some amount of future cash committed to players, all of it done before the coronavirus pandemic swept the globe. There are several different ways to look at salaries; for instance, for purposes of calculating the luxury tax, the average annual value is the touchstone, with up-front bonuses spread over the life of the deal. For this exercise, we’ll focus on actual cash outlays that still have yet to be paid.

We’ll run through every team, with a big assist from the Cot’s Baseball Contracts database. Prior entries can be found here. Next up is the Pirates:

*Includes buyouts on club options over Chris Archer and Gregory Polanco

*Does not include remaining contractual obligations to Felipe Vazquez (on restricted list and facing multiple criminal charges in multiple jurisdictions)

(click to expand/view detail list)

Creative Playoff Expansion Can Get a Deal Done

Dr. Matt Swartz is a Labor Economist who has researched and published on MLB labor markets for over a decade at websites including The Hardball Times, FanGraphs, and Baseball Prospectus, as well as at MLB Trade Rumors. Matt created the arbitration salary projection model for MLB Trade Rumors, and co-created the SIERA pitching statistic available at FanGraphs. He has consulted for a Major League team since 2013, in addition to working in his day job as an economist in the cable industry. This article reflects his own opinion and not that of any of his employers or clients.

Previous posts: Resolving This Player-Owner Dispute Should Be Easy; MLB Collective Bargaining and Risk Sharing.

There is a way that players can get prorated salaries for a 72-game regular season and the owners can make enough money to only pay the equivalent of 68% of prorated salaries. We know the way that owners will agree to a deal with prorated salaries for 2020; they insist they need the revenue to make up for losses incurred during the regular season. While both owners and players have proposed expanded playoffs as a way to increase that revenue, they have been unable to create enough revenue for the owners to bite. I have a solution for this problem—start the playoffs earlier, add playoff teams, make the series longer, and reap the extra television revenue. There is more than enough there to get a deal done.

The biggest roadblock to completing a deal is the combination of the union’s insistence that players be paid on a prorated basis per regular season game, and the owners’ insistence that players take less than their prorated salaries due to absence of fans in the stands. Players have shown a willingness to extend the playoffs—effectively playing some games for free. Owners have shown some willingness to put on a 50-game shortened season with typical playoff structure, but have balked apparently at the risk of the players filing a grievance for not putting on as long a season as possible.

Eugene Freedman tweeted to me earlier in this series that the reason players were so insistent on prorated salaries is to avoid precedent. If this is true, the only way around this is finding more revenue sources—something the player proposals have hinted at, but not provided adequately to appease owners.

The owners have repeatedly centered on completing the regular season by September 27 and the World Series by the end of October, fearing that a second wave of COVID-19 in the fall could preclude the playoffs.

Fans have an additional concern that my proposal would resolve—they want to make sure that the World Series Champion deserves their title. A shortened season, combined with expanded playoffs, naturally increases the possibility that a mediocre team could walk away with the crown.

They could solve this by ending the regular season 10 days early to end on September 17, using doubleheaders and other ways to get to 72 games (or just shrinking the season further if the players are amenable). Then they would have 10 extra days to get in a lot more playoff games.

My proposal is that playoffs are expanded to 16 teams, but that all 15 series are Best-of-Seven series. On average, this will increase the expected number of nationally broadcast playoff games from 36 to 90 – a whopping increase of 150%. With $787 million reportedly at stake in television revenue for those 36 playoff games, it stands to reason that networks would pay at least half as much for the addition 54 games as the original 36, which brings in something like a whopping $590 million in extra revenue.

If players are content to simply get by on prorated salaries for 72 regular season games, they would receive about $1.84 billion in revenue. The owners’ extra playoff revenue places them in the equivalent position of 68% of prorated salaries. Marginal costs of operating these games are probably small enough to keep this only a couple percent higher. The owners almost certainly need the players to take a haircut smaller than 32%, so there is plenty of room for give in this approach. Even if networks were only willing to pay a third of the per-playoff-game rate, that would still be enough revenue to get owners to effectively pay the equivalent of 79% of prorated salaries. There is probably even room in there to give the players some playoff share, cover some marginal costs of games, and other things that could be required for this to be profitable to owners and acceptable to players.

As a result, the odds that an inferior team wins a given series are lower, and it becomes more likely that a deserving champion is crowned. The league could even take further advantage of the empty-stadium format by tilting home field advantage entirely towards the team with the superior regular season record.

I have researched home field advantage extensively, and have learned that rather than home crowd support or even last at-bats, the real reason home field advantage exists is that players are more familiar with their own parks. Teams who are home for a 7-game series will have a 59% chance of winning an evenly matched series already. A superior team certainly could easily have a 70% chance of winning a series in many cases.

This seems to be something that would accomplish the requisite situation for all parties, and there are many other ways that players could help teams add revenue without sacrificing their prorated salary demand. But the key is many more playoff games, since that is the only way owners make back losses they claim from the regular season, and the only way players do not have to surrender their principle of prorated salaries.

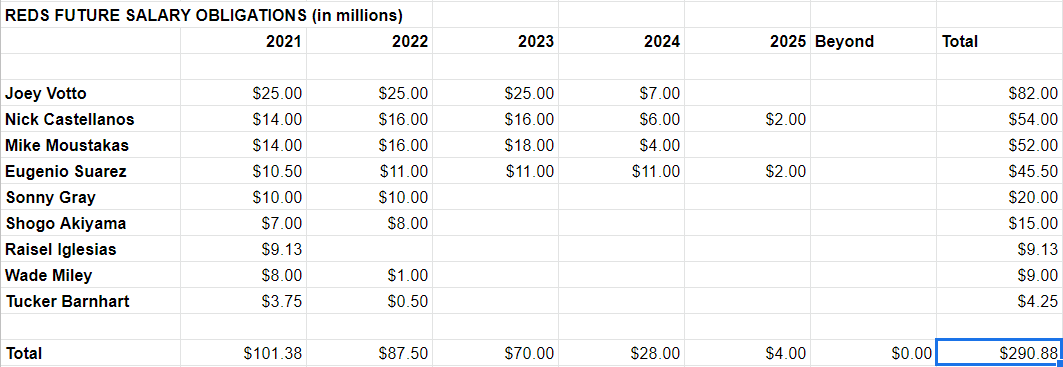

Reds Have Nearly $300MM In Post-2020 Payroll Promises

2020 salary terms still need to be hammered out. But what about what’s owed to players beyond that point? The near-term economic picture remains questionable at best. That’ll make teams all the more cautious with guaranteed future salaries.

Every organization has some amount of future cash committed to players, all of it done before the coronavirus pandemic swept the globe. There are several different ways to look at salaries; for instance, for purposes of calculating the luxury tax, the average annual value is the touchstone, with up-front bonuses spread over the life of the deal. For this exercise, we’ll focus on actual cash outlays that still have yet to be paid.

We’ll run through every team, with a big assist from the Cot’s Baseball Contracts database. Prior entries can be found here. Next up is the Reds:

*Includes buyouts on club options over Joey Votto, Mike Moustakas, Eugenio Suarez, Wade Miley, and Tucker Barnhart

*Includes deferrals and buyout on mutual option in Nick Castellanos contract; Castellanos may opt out after 2020 or 2021

(click to expand/view detail list)

MLB Collective Bargaining and Risk Sharing

Dr. Matt Swartz is a Labor Economist who has researched and published on MLB labor markets for over a decade at websites including The Hardball Times, FanGraphs, and Baseball Prospectus, as well as at MLB Trade Rumors. Matt created the arbitration salary projection model for MLB Trade Rumors, and co-created the SIERA pitching statistic available at FanGraphs. He has consulted for a Major League team since 2013, in addition to working in his day job as an economist in the cable industry. This article reflects his own opinion and not that of any of his employers or clients.

In essence, every proposal floated by the owners has requested that players assume the downside risk associated with lower ticket revenue. Part of the reason I suspect this is offensive to players is that owners have benefited substantially in recent years from upside risk associated with television revenue, and little to none has found its way into player salaries.

To understand why, all we need is a superficial understanding of labor economics. Baseball’s free agent market follows those models better than perhaps either side realizes. Owners offer free agents certain salaries because they believe that their labor will generate as much money in revenue. Yet owners primarily get their revenue from two sources: tickets and television.

Since what free agents are actually selling is wins, the translation from ticket revenue to free agent salaries is obvious. Teams sell more tickets when they win more games. Especially if those wins push them further in the playoffs, they sell substantially more season tickets in subsequent seasons. Teams readily pay free agents with this in mind.

Yet the translation from television revenue to free agents is virtually nonexistent. National television deals with ESPN, TBS, and FOX are distributed to all teams, regardless of how many games they win. Regional Sports Networks often sign multi-decade contracts with teams to broadcast their games, which also are unaltered by win totals in a given season.

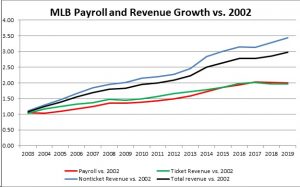

The reason this matters, and the reason this is a source of acrimony between the owners and players now, is that television revenue has grown far more quickly than ticket revenue. Player salaries have grown in magnitude about as much as ticket revenues have— suggesting this theory is likely true. Owners have seen higher profits from faster growing television revenue.

Consider my rough estimates in the graph below. Here I have used Baseball Prospectus payroll totals, approximate average ticket prices from various sources, average attendance from Baseball Reference, and Maury Brown’s (now unavailable) BizOfBaseball.com website and Forbes articles for total revenue. None of these figures are exact but they are certainly close enough that the message and pattern is obvious. Players have seen salary growth (red) almost exactly in accordance with the growth rate of ticket revenues (green), while owners’ profits have grown more quickly as they pocket the faster-growing television revenue (blue). This is not the owners pulling the wool over the union’s eyes—it is just the structure of their agreements in which the payroll share of revenue is not fixed as it is in other sports, but tied to owner incentives that have not kept up with total revenue.

If the owners want the players to accept the downside risk associated with low ticket revenue, they need to find a way to share the upside risk associated with higher television revenue.

A starting point is simple. Instead of minimum salaries defined exactly by the CBA, let free agent and arbitration prices be set in excess of the salary minimums, and set future salary minimums distributed to all players. Let those minimums represent some fixed X% of the cumulative national television deals. Bargain about that percentage, but when TBS offers 40% more in their next deal than their current deal, players will see that upside. In exchange, when future identifiable events lower ticket revenue— e.g. say government regulations of Y% reduced capacity in stadiums due to COVID-19 in 2021– the players will accept lower salaries by Z%. This gives players exposure to upside and gives owners protection from downside. Everything else is bargaining around X, Y, and Z%.

Now is the time for the players to request this. Now is the time for the owners to offer this. It need not even be for 2020– that ship may have sailed already. By right now, there is downside risk associated with empty seats associated with 2021. If owners want players to assume lower salaries in such a situation, they should make an offer to give the players a piece of future television revenue growth now. Otherwise, the players will again be asking the owners the same question next year: “Why should we accept this downside risk?”

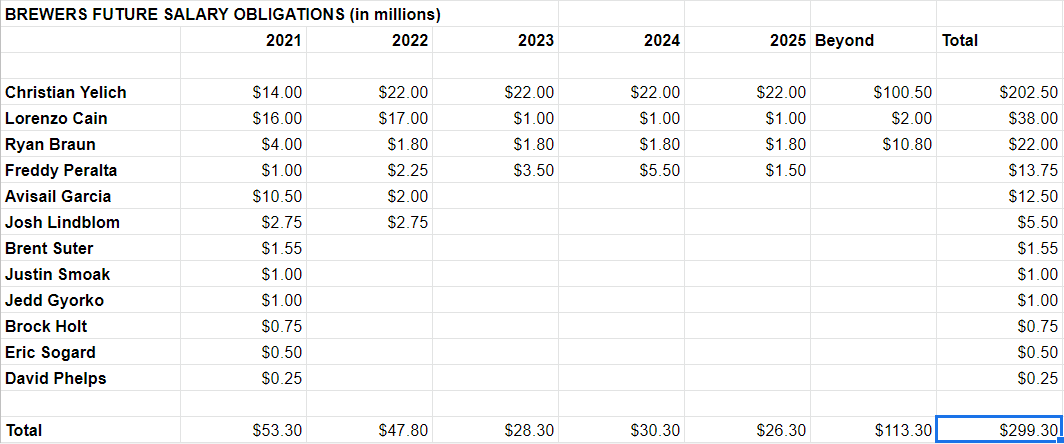

Breaking Down The Brewers’ Interesting Slate Of Future Contracts

2020 salary terms still need to be hammered out. But what about what’s owed to players beyond that point? The near-term economic picture remains questionable at best. That’ll make teams all the more cautious with guaranteed future salaries.

Every organization has some amount of future cash committed to players, all of it done before the coronavirus pandemic swept the globe. There are several different ways to look at salaries; for instance, for purposes of calculating the luxury tax, the average annual value is the touchstone, with up-front bonuses spread over the life of the deal. For this exercise, we’ll focus on actual cash outlays that still have yet to be paid.

We’ll run through every team, with a big assist from the Cot’s Baseball Contracts database. Prior entries can be found here. Next up is the Brewers:

*Includes deferrals in Christian Yelich and Lorenzo Cain contracts

*Includes deferrals and buyout on mutual option in Ryan Braun contract

*Includes buyouts on club options over Freddy Peralta, Avisail Garcia, Justin Smoak, Jedd Gyorko, Brock Holt, Eric Sogard, and David Phelps

(click to expand/view detail list)

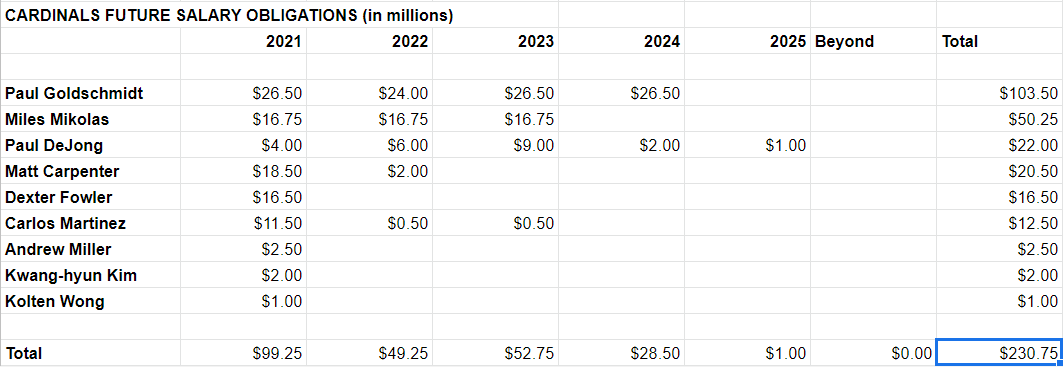

Calculating The Cards’ Future Contract Guarantees

2020 salary terms still need to be hammered out. But what about what’s owed to players beyond that point? The near-term economic picture remains questionable at best. That’ll make teams all the more cautious with guaranteed future salaries.

Every organization has some amount of future cash committed to players, all of it done before the coronavirus pandemic swept the globe. There are several different ways to look at salaries; for instance, for purposes of calculating the luxury tax, the average annual value is the touchstone, with up-front bonuses spread over the life of the deal. For this exercise, we’ll focus on actual cash outlays that still have yet to be paid.

We’ll run through every team, with a big assist from the Cot’s Baseball Contracts database. Prior entries can be found here. Next up is the Cardinals:

*Includes remaining bonus payments owed to Paul Goldschmidt, Miles Mikolas, and Dexter Fowler

*Includes buyouts on club options in Carlos Martinez, Paul DeJong, Matt Carpenter, Andrew Miller, and Kolten Wong contracts

(click to expand/view detail list)

Resolving This Player-Owner Dispute Should Be Easy

Dr. Matt Swartz is a Labor Economist who has researched and published on MLB labor markets for over a decade at websites including The Hardball Times, FanGraphs, and Baseball Prospectus, as well as at MLB Trade Rumors. Matt created the arbitration salary projection model for MLB Trade Rumors, and co-created the SIERA pitching statistic available at FanGraphs. He has consulted for a Major League team since 2013, in addition to working in his day job as an economist in the cable industry. This article reflects his own opinion and not that of any of his employers or clients.

The MLB Owners and MLB Players Association have been unable to reach an agreement for the financial terms of the 2020 season, and at this point they may not reach one at all. Both sides have focused publicly on the morality of their case, each believing they have the ethical upper hand. Neither has made proposals that reflect their actual negotiating position. That the arguments have primarily focused on morality is perhaps not surprising, but it doesn’t create fertile ground for an actual substantive negotiation. I studied bargaining theory, and I don’t remember anything about how to win a moral argument. The ethics are what they are, and any reasonable person could make either side’s case if they really tried. The union seems to be winning the PR war thus far, as fans seem to mostly blame owners, but supportive tweets from fans are not convertible into currency.

At its core, what we have is the following set up: The presumptive default position, if no agreement is reached, is that commissioner Rob Manfred will order a roughly 50-game season with full prorated salaries. If the sides do reach an agreement, they may play as many as 80 games, and be able to split the associated revenue. They also may be able to add revenue through other avenues like expanded playoffs, and they could split that revenue too. Those are the gains from a negotiated agreement. They can be split in a way to make both parties better off.

Both sides have accused the other of not bargaining in good faith, but neither side has offered the other side anything they would plausibly accept. Instead we have seen the owners repeatedly try to offer players only slightly more than the same salary total as they would with a 50-game season, effectively asking for all the gains that would accrue from a negotiated agreement while leaving the players to absorb greater output and greater risk (both from the usual risk of playing baseball and the additional risk attendant to the global pandemic). The players similarly have failed to offer the owners anything that would lead to more profit than they would accrue in the event of a 50-game season with unexpanded playoffs. It is not surprising negotiations have gone nowhere.

At this point, an agreement for a better, longer season in 2020 is doubtful. But 2021 is right around the corner, and there is no vaccine for COVID-19 yet. We may not see fans in the seats in 2021, or at least we may not see stadiums filled to capacity. So we may see a replay of this argument in 2021 as well. It’s imperative that both sides recognize their position and negotiate accordingly. This acknowledgement could easily flip the script and lead to an expedited deal for 2020 already.

Let’s start with what should be obvious and unarguable.

Unarguable Point A:

Any agreement should see the players earn substantially more than they would have in a 50-game season.

Unarguable Point B:

Any agreement should see owners make more profit than they would in a 50-game season.

Nothing floated publicly has even come close to meeting these simple criteria.

The starting point here is actually fairly simple. Forget about inching towards a middle ground when neither side is willing to budge. Instead, begin by figuring out just how much extra revenue is associated with 30 extra games and an expanded postseason. Then, split it in half. The players’ salary total is equal to that half plus their prorated salaries for 50 games. Both sides may try to argue for a bigger piece of the pie, but either side would be crazy to say no to half of this revenue—which is much more than the zero extra revenue they would see otherwise. The players don’t need the owners to open their books on any more than is necessary to estimate this amount. The owners don’t need to ask the players to sign any waivers or anything else that isn’t already negotiated. Anything on top of this baseline can be negotiated after setting the above in writing and shaking hands (but not actually).

Offers could get more complicated and cover more territory. This is especially true with the risk of no fans or fewer fans in 2021, and with the CBA expiring after 2021. But the essential 2020 issue can be resolved in a fairly simple manner that makes each side better off in the short term while limiting the long-term damage to the sport. In subsequent pieces, I’ll discuss the fundamentals of baseball’s free agent market and how players might want to approach the inequities that have arguably developed over the last couple years. But for now, let’s just agree that owners, players, and fans can all be made much better off very quickly. Get it done before dinnertime.

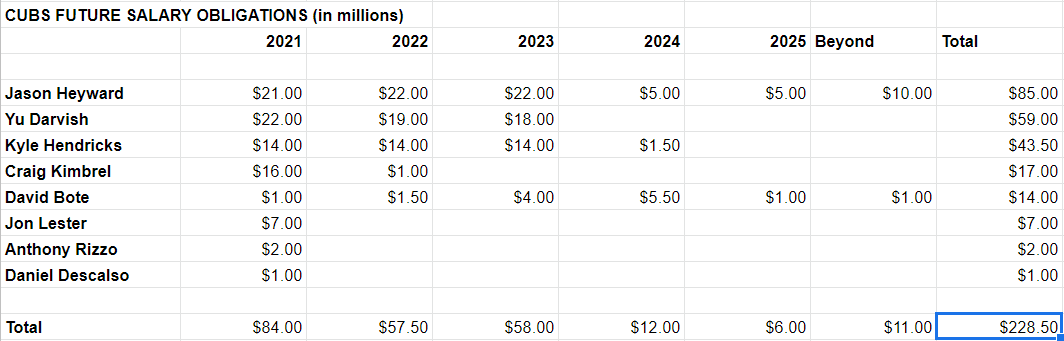

What Do The Cubs Owe Players After 2020?

2020 salary terms still need to be hammered out. But what about what’s owed to players beyond that point? The near-term economic picture remains questionable at best. That’ll make teams all the more cautious with guaranteed future salaries.

Every organization has some amount of future cash committed to players, all of it done before the coronavirus pandemic swept the globe. There are several different ways to look at salaries; for instance, for purposes of calculating the luxury tax, the average annual value is the touchstone, with up-front bonuses spread over the life of the deal. For this exercise, we’ll focus on actual cash outlays that still have yet to be paid.

We’ll run through every team, with a big assist from the Cot’s Baseball Contracts database. Prior entries can be found here. Next up is the Cubs:

*Includes remaining bonus payments owed to Jason Heyward

*Includes buyout on club options in Kyle Hendricks, Craig Kimbrel, David Bote, Anthony Rizzo, and Daniel Descalso contracts

*Includes buyout on mutual option in Jon Lester contract

(click to expand/view detail list)